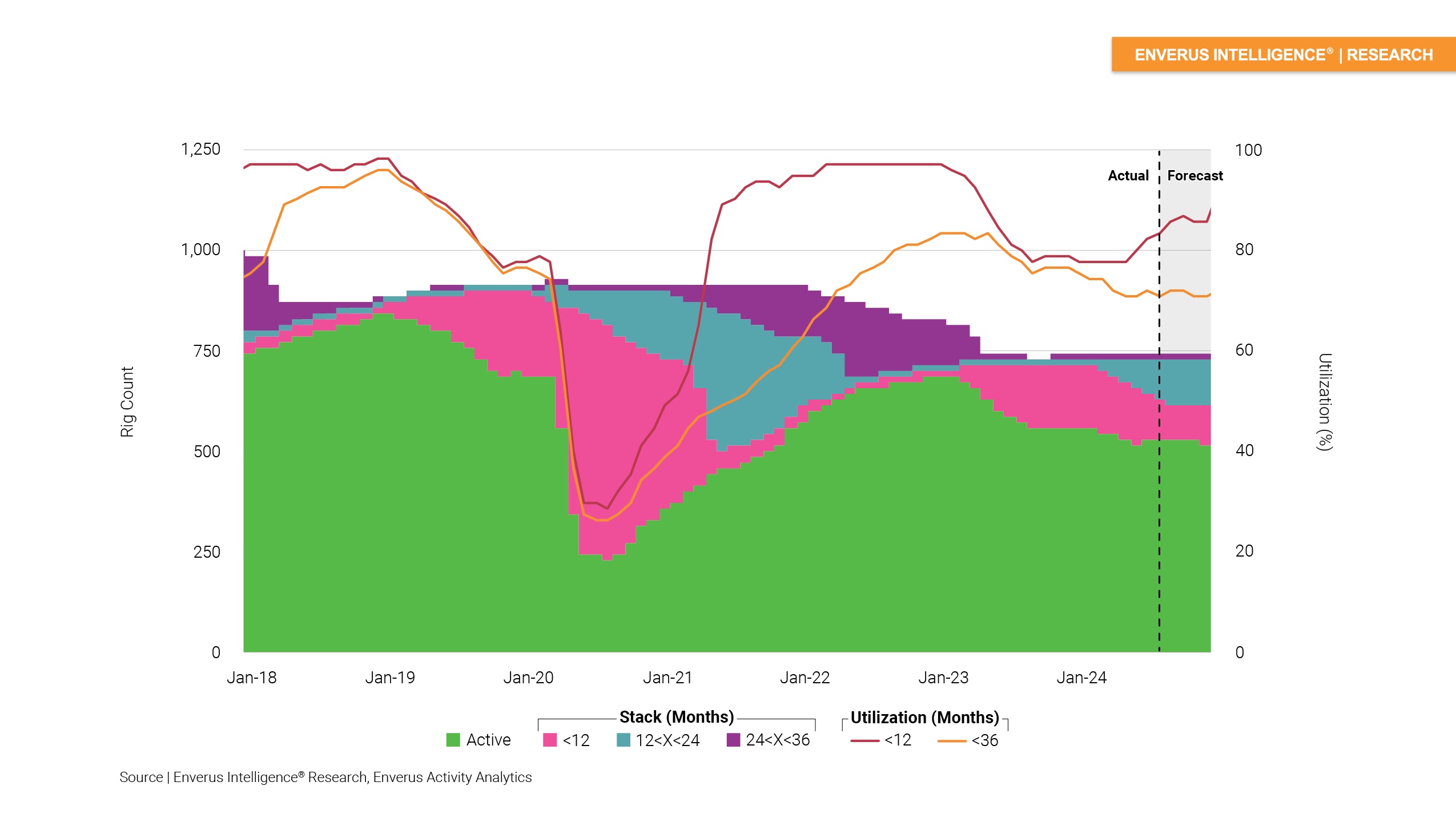

Enverus Intelligence Research, a subsidiary of Enverus, an energy-dedicated SaaS company, released on Oct. 1 its Oilfield Services Market Fundaments report that examines supply and demand dynamics in each service line. EIR also forecasts changes in year-end costs to coincide with E&P budgeting season. “We believe activity has bottomed and oilfield service price will bottom by the end of this year, and EIR expects a modest rebound in activity and pricing in 2025,” said Mark Chapman, report author and OFS principal analyst. “An oversupply of fracture sand caused prices to fall this year, but an expected rebound in gas-directed drilling and a trend to longer laterals should boost prices in 2025.” Among the key takeaways of the report: Shale well costs are expected to decrease by 6.3 percent in 2024 due to lower activity and increased efficiencies. Costs will rise 2.8 percent in 2025 with increasing activity and higher demand for new drilling technology. The pressure-pumping market shows a large divide, with high demand for electric fleets and Tier 4 dual-gas blend rigs, while diesel equipment faces challenges. Fracture sand supply increased in 2Q24, leading to price softness, but demand is expected to rise in 2025 due to longer laterals and a rebound in gas-directed drilling.