President Trump is calling on OPEC to increase U.S. crude production, which could easily push crude prices lower into this second quarter of 2025, as supply would likely then outpace demand. Just how low could prices go—or will they fall at all? The answer depends on a confluence of factors, as supply is just one part of the equation.

Economic Slowdown Still a Risk

For instance, another fear haunting crude is the stubborn 10-year Treasury yield currently hovering just over 4.5 percent. If 10-year yields drift north of 5 percent, it would very likely create the economic slowdown that most economists once predicted but have now reneged on. Although the U.S. stock market highs that investors have enjoyed make it easy to ignore this possibility, keep in mind that the last two years of the S&P 500 posting returns north of 23 percent each year are not sustainable. That’s especially true given the fact that a handful of stocks known as the “Magnificent 7” anchored these gains, rather than performance being spread out within the index.

And then there’s China to consider. The Chinese economy struggled throughout 2024 despite government stimulus to try to jump start growth. As China is still the “manufacturer of the world”—and thus the second-largest oil consumer—continued economic slowdown in China would negatively impact global oil demand. Along these lines, if we add the declining demand situation from China to the other factors above, it’s easy to justify the view that crude prices may decline.

At the same time—the prospect of more Chinese economic stimulus, combined with potential sanctions on Iranian and Russian oil—have been encouraging hedge fund investors to increase their bullish positioning on U.S. crude. Although these bets may at first seem to support the view that higher U.S. crude prices are to come, it’s also important to keep in mind that they place the market in a vulnerable position. In other words, there could be a significant price drop in the market if traders who previously bet on the price going up are now forced to sell due to a sudden downturn, causing further selling pressure and accelerating the price decline.

Effects of Trump Administration’s Policies Remain to be Seen

Many speculated that President Trump taking office would impact the energy industry—and even in just the first few weeks of his term, he announced policies and plans that could indeed impact crude prices. Most directly, he said he plans to re-fill the U.S.’s Strategic Petroleum Reserve (SPR) “right to the top and export American energy all over the world.” This plan to re-fill the SPR—and do it quickly—could create a buying floor for crude, and purchases could step up very quickly if the price of West Texas Intermediate (WTI) falls significantly.

Furthermore, the Trump administration’s policies on tariffs could be both a positive for crude prices and a negative depending on who bears the brunt. Tariffs on imports from oil-producing countries would likely restrict supply, driving prices higher. Meanwhile, tariffs on imports from countries with heavy demand for crude, such as the tariff on Chinese goods, could easily slow those countries’ economies, creating less demand. Initially, U.S. gas prices rose on the news that the U.S. was imposing tariffs on Canada, Mexico, and China, but then fell again on Feb. 3 after the tariffs on Mexican and Canadian goods were paused. Around 25 percent of the crude that comes into the United States is from Canada and Mexico.

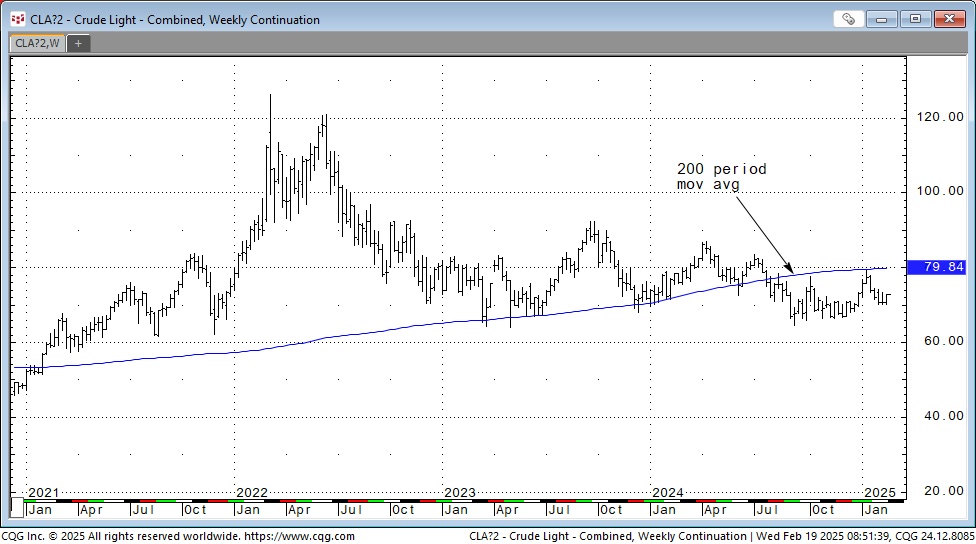

This chart from cqg.com tracks WTI crude futures prices over the past four years.

How other countries respond to these tariffs is also a question mark. Immediately after Trump made the announcement, Canada responded by putting 25 percent tariffs on some American goods, such as alcohol and perfume, but Trump pivoted and delayed the tariffs for 30 days, so Canada paused theirs as well.

And so, what’s ahead? Well, looking from a longer-term technical outlook the trends have been retracing lower for WTI crude futures. The longer-term weekly chart, which sets moving averages below both the 100 and the 200 period, is possibly trending back towards the $65-per-barrel area. While the trend is lower, keep in mind that the fundamentals of supply and demand draw the charts, and the fundamental outlook is definitely a moving target in each coming week as the Trump Administration settles in further.

How are Capital and Bank Markets Working for O&G?

In 2024, the wave of acquisitions continued. The narrative hasn’t changed with public companies looking to add inventory and scale to stay relevant. In this favorable environment, private companies in multiple basins realized significant returns for their investors by exiting their commitments.

The buyers, mostly public companies, finance these acquisitions with cash on hand, stocks, and occasionally bank and public debt. Exploration and production companies (E&Ps) continued to focus on healthy balance sheets and capital discipline, providing buyers with liquidity and access to public high-yield debt at reasonable rates.

The banks felt significant payoff pressure last year. As we enter 2025, many reserve-based lenders are looking for opportunities to redeploy debt capital to the sector. This has led to more favorable debt terms for borrowers, as banks are becoming more aggressive to win business. Existing borrowers are operating with less debt relative to their EBITDA; therefore, debt dollars are available to fund acquisitions and development.

From an equity standpoint, the recent sales have increased the need to fund new upstream and midstream companies. With several funds closing and potential co-invests from LPs, sponsors and their management teams are hungry for assets. There are many buyers on the sidelines driving valuations up. These higher valuations should encourage public E&Ps to divest non-core positions. As finding large positions has become increasingly difficult, we are also seeing revived activity in basins such as the Mid Continent, Rockies, Williston, and Eagle Ford, which have not had the same activity level as the Permian over the past several years.

Traditional large sponsors have generally found it difficult to fund small to mid-market opportunities, creating pressure on prices for assets valued above $500MM. Mid-size private equities, family offices, and new entrants have been actively looking for smaller deals and, in some cases, a lease and drill strategy. Another equity trend is the renewed interest in initial public offerings (IPOs), which provide another exit strategy for private companies in addition to a sale.

Overall, capital is available on the debt and equity sides. Prices and valuations are currently supporting deal-making, and ultimately, the desire for large companies to divest non-core will be the catalyst for putting these dollars to work.

Dennis Kissler

Paul Edmonds

Dennis Kissler is Senior Vice President of the Trading Division at BOK Financial’s office in Oklahoma City. Paul Edmonds is Senior Vice President of Energy Financial Services at BOK Financial’s office in Houston.