In this month’s collection of articles, the predominance of the Permian Basin continues to figure into any discussion of domestic energy, and even world energy. These are the full versions of the “Drilling Deeper” news items that appeared as abbreviated versions in the print edition of PB Oil and Gas Magazine’s June 2019 issue.

Permian Basin to Lead Growth,

Per New GlobalData Study

Abundant hydrocarbon reserves and the ability to drill longer laterals has made Permian Basin the most prolific shale play in the world, according to GlobalData, a leading data and analytics company. The company’s latest market analysis report, “Permian Basin Shale in the United States, 2019—Oil and Gas Shale Market Analysis and Outlook to 2023,” reveals that production of crude oil and natural gas has grown each year from 2013 to 2018 despite the oil and gas industry going through one of the worst downturns during that period.

The Permian Basin is one of the largest structurally developed basins in the United States. Shale formations in the Permian Basin can range from 1,300 feet to 1,800 feet in thickness, making it one of the thickest deposits in the world.

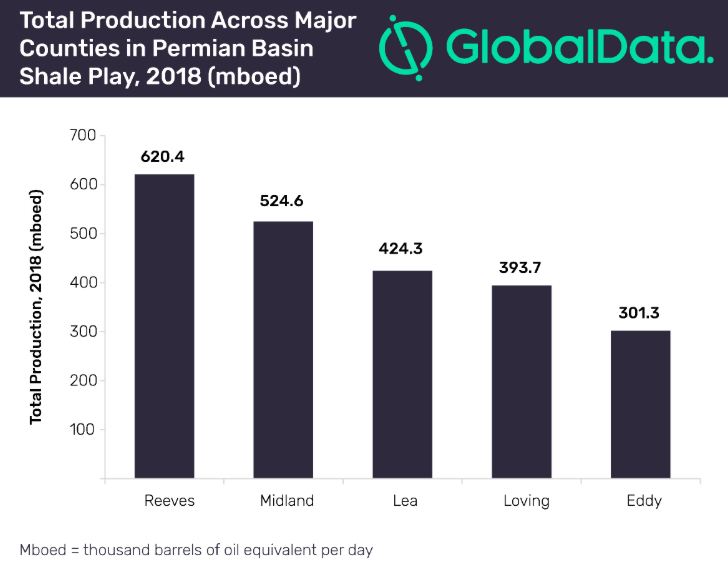

GlobalData identifies companies such as Occidental Petroleum, Chevron Corporation, Pioneer Natural Resources, Concho Resources, and EOG Resources as among the leading producers in the Permian Basin shale in 2018. The major hydrocarbon producing counties in the Permian Basin include Reeves, Midland, Lea, Loving, and Eddy.

As in other unconventional shale plays, operators in the Permian Basin continue to drill longer laterals beyond 9,000 feet, with some reaching as much as three miles. The general objective remains to increase the productivity of the new producing wells in a higher proportion with respect to the cost increase associated with these more complex wells.

The Permian has also seen a clear trend for larger scale operations of key operators that increase the surface of continuous acreage and allows for more recovery. This has also driven the M&A activity in the Permian, with companies like Chevron, Diamondback Energy, and Concho Resources looking to expand their Permian footprint to drive greater efficiency and lower production cost.

Adrian Lara, Senior Oil and Gas Analyst at GlobalData, comments: “Permian crude oil production increased by more than one million barrels per day (mmbd) in 2018, and by early 2019 it has already surpassed the four mmbd mark. However, the story for natural gas production is somewhat different, largely because an increasing volume of associated gas has been flared due to limitations in the pipeline capacity. If the capacity constraints persist longer, it may force some operators to shut in their wells.”

The limitations to gas pipeline capacity that gave rise to flaring is estimated to ease during 2019–2020, with approximately four billion cubic feet of pipeline capacity expected to be added during these two years, giving further lift to Permian production.

Lara concludes: “In spite of the infrastructure bottlenecks Permian acreage remains highly attractive. Whenever possible, operators try to increase the surface of continuous acreage that would allow for larger scale developments and longer well laterals. This is in fact one of the key drivers behind the recent offers made by both Chevron and Occidental Petroleum to acquire Anadarko’s acreage. Whichever company ends up winning the deal will certainly establish a leading position among the top players in the play.”

United States to Lead Crude Gains

Among Non-OPEC Nations

New analysis released by Fitch Solutions reveals that the United States will lead gains in non-OPEC crude oil production over the next several years as crude prices recover. In the gas market, a ramp-up in production will respond to growing capacity from LNG export facilities and petrochemical plants. Fuels

consumption growth will decline over the next decade as efficiency gains take root.

Latest Updates And Key Forecasts

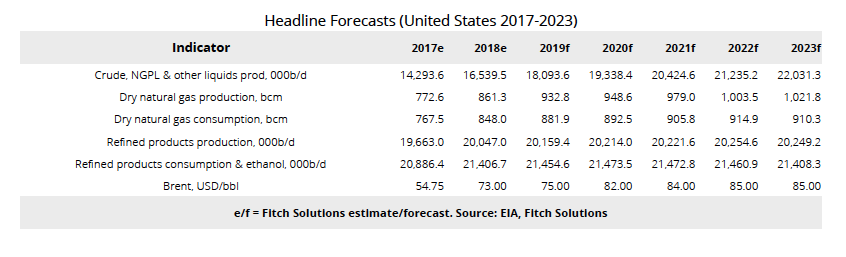

• We maintain our oil Brent price forecast this quarter at USD73.0/bbl. We expect WTI will average USD65.0/bbl in 2019. Volatility has begun to creep back into the market and there are early signs that investors are tilting back towards safe havens.

• U.S. crude production will extend its recovery in 2019. We expect total U.S. liquids will grow by an average rate of 9.4% y-o-y versus a 15.7% gain in 2018. In 2018, crude production rose by nearly 1.6mn b/d, an all-time record. In 2019, we expect crude will grow by just under 1.3mn b/d.

• Natural gas production will rise in response to growing export capacity. We project an 8.3% y-o-y expansion, averaging 932.0bcm, up from an average of 861.3bcm in 2018.

• Producers will move away from drilling mature assets or vertical low-yielding wells in tight formations in favour of maximizing returns from core acreage. This will encourage companies to explore longer laterals across consolidated positions, exceeding a previous industry limit of 3.0km (10,000ft) into the 4.0-4.5km (13,000-15,000ft) range.

• Larger E&Ps with substantial in-house capabilities will generate the bulk of overall growth in 2019. Companies such as EOG, Occidental Petroleum, and Anadarko have secured strategic components of the value chain that lower operational costs and facilitate future growth.

• The Permian basin will continue to outperform, given its strong connectivity to major refining and export infrastructure. We expect the play will contribute approximately 800,000b/d of incremental crude output in 2019. The Bakken formation will slow as a result of insufficient takeaway capacity, adding just over 200,000b/d of output. These gains will propel the shale sector beyond the 8.0mn b/d mark, representing a 15.7% y-o-y increase.

• The Trump administration announced plans to loosen offshore drilling regulations that were put in place after the 2010 Deepwater Horizon oil spill to prevent another disaster. The new rules — one of which will reduce testing requirements for safety devices called blowout preventers — were announced by former oil lobbyist and acting Interior Secretary David Bernhardt and detailed in a 289-page plan.

• President Trump has opted not to renew the 180-day US sanctions waivers that were awarded back in November to key buyers of Iranian crude. These waivers expire on May 2, at which point exports should – in theory – drop to zero. It appears that he is gambling that the sharp decline in Iranian exports will not lead to any significant increase in the price of crude.

• LNG export capacity is expected to grow following ExxonMobil’s final investment decision for the Golden Pass project in February. The USD10.0bn project will have a liquefaction capacity of 15.6mn tpa across three trains and is expected to begin service in 2024.

• In April, Tellurian announced that the US Federal Energy Regulatory Commission issued the order granting authorisation for Driftwood LNG, a proposed 27.6mn tonnes per annum (mntpa) liquefaction export facility near Lake Charles, La., and the associated Driftwood pipeline, a 96-mile proposed pipeline connecting to the

facility.

• The return to Democratic control of the US House of Representatives following the midterm elections will constrain the Trump administration’s ability to roll back regulations targeting the oil and gas sector.

Capital Discipline, Spending

Hold Keys to 2019, Per Execs

Shifting oil and gas industry forces mean that capital discipline, decreased spending and consolidation will continue to mark the industry in the coming years, say oil and gas and finance executives addressing about 150 attendees at the annual BoyarMiller Energy Breakfast Forum, held April 29 in Houston, Texas.

“Our speakers agree that we are currently in the middle of the latest oil and gas cycle and while oil prices have been recovering, there are substantial changes taking place that will have a long-term impact on the industry,” said Chris Hanslik, chairman of BoyarMiller. “Our moderated discussion was packed with an inside look at the challenges and opportunities occurring within this vital industry to Houston.”

The three speakers at the BoyarMiller Energy Forum included Laura Schilling, president of Pumpco Services; Matt McCarroll, chairman and CEO of Fieldwood Energy LLC; and James P. Baker, managing director and global co-head of investment banking and capital markets at Piper Jaffray & Co.

Call for capital discipline

“What’s happening right now is that oil prices have been recovering since the lows of last December, but E&P spending is actually down in the US onshore market year over year,” said Schilling of oilfield services (OFS) company Pumpco Services. “And even though there is a constructive trajectory of oil prices for the rest of the year, there is a call for capital discipline to the E&P companies, as well as OFS, to drive greater cash flows which is changing the dynamics of this cycle. Investors are voting with their wallets and energy is currently less than six percent of the S&P 500.”

Schilling said both the operators and the OFS segment of the industry are expected to provide investors and shareholders a return through dividends and buy backs, and OFS companies with debt are working to improve balance sheets.

“The focus in OFS right now is free cash flow and that is how we are going to bring investors back and build sustainability,” said Schilling.

To do that, Schilling said the OFS sector has to embrace a “new normal” that could be different from the previous business models.

“You either have to work the efficiency side of the business, like a Southwest Airlines model, or you need unique technological differentiation. In the completions market, there are a lot of players and those in the middle that do not differentiate will not survive,” said Schilling. “We are focused on efficiency. Given the rising complexities of wells today, some of this is back to the basics of performing well for operators and that will continue to earn market share going forward.”

A tipping point

Schilling also said the industry’s new normal includes the adoption of “big data” as operators work with Google, Amazon and Microsoft to gain information about improvement of field operations, equipment, and well management.

“Integrating data and algorithms from these companies into operations improves decision making and is going to be essential in the future as operators strive to reduce costs,” said Schilling. “We have sensors on much of our equipment for predictive maintenance and real-time analytics and it has been phenomenal. The tipping point is here in utilizing new software, cloud platforms for remote operations, and other technology—and it’s exciting to see.”

Even with the industry’s advancement of technology and adoption of big data, Schilling said there is still one key component to success.

“Execution matters. For instance, at the Permian Basin there are multiple vendors operating onsite and activity must be coordinated to move massive pieces of equipment every day to achieve efficiency for the operator, and to do it safely,” said Schilling. “So technology is important but execution wins the game.”

Segmentation and spending

Matt McCarroll of Fieldwood Energy believes the industry is more segmented today and cited his private company as an example of how it is different from large and onshore operators.

“We are going to spend more capital during the next 12 to 18 months than we have spent over the last five years,” said McCarroll who attributed increased spending to the company’s work in the deepwater Gulf of Mexico that will amount to 50,000 barrels of production over the next two years. “But it is a challenging time. You won’t ever see again the activity levels of 2005 when there were 80 active operators in the Gulf. At the Gulf of Mexico lease sale a few weeks ago, there were only 30 companies that made bids. There has been a lot of consolidation and the industry in the Gulf has fundamentally changed.”

He addressed the concerns about efficiency among operators citing services provided at a reduced day rate are only effective if executed safely and efficiently.

“While costs have come down substantially, and day rates have dropped, if it takes twice as long to drill because the equipment has not been serviced recently or the crew is not well trained, there are no savings. People misconstrue that because rates are down, there is more money being made,” said McCarroll. “We look for the highest quality vendors that will help us produce most efficiently.”

McCarroll also addressed the challenges private producers face in planning a profitable exit strategy.

“The traditional exit for private equity is a strategic buyer or going public, but it is difficult to go public today. As a private company with stakeholders, including private equity, you need liquidity at some point. We are looking at different options to reach

that goal,” said McCarroll.

McCarroll doesn’t make predictions about oil prices and said you can get caught up trying to over-analyze oil prices. “If I knew where oil prices were going I wouldn’t be producing it, I’d be trading it,” he joked with the audience.

Shifts in funding

James Baker of Piper Jaffray & Co. addressed the new landscape for buyers and sellers in the midstream sector.

“The biggest change in the midstream space is that 10 years ago the vast majority of buyers were master limited partnerships or MLPs,” said Baker. “Since 2017, we have seen about $50 billion worth of mergers and acquisitions in midstream; approximately $40 billion of it has been financial buyers with $10 billion representing strategic buyers.”

According to Baker, the industry is seeing a market trend where MLPs are converting to C Corps because of the sharp reduction in the U.S. corporate tax structure and the ability to access a larger base of institutional investors. “It’s a much bigger pool for companies when they get back to growing and need to raise capital,” he said. “But many institutional investors look at the industry and say there are too many midstream companies that look the same and there needs to be consolidation—and that’s not an easy solution.”

“The entire business model has changed for upstream private equity groups,” said Baker. “Traditionally, they have backed a management team to go out and lease acreage, prove it, and then flip it to a strategic. That market has disappeared. Now they have to hire operators and run it as a company and within cash flow or maybe push until an exit appears. It’s a totally different approach.”

Baker concluded stating the investment community has shifted from a focus on growing production, to a focus on capital discipline and financial metrics that require a different mindset.

For more information about the BoyarMiller Energy Forum, visit boyarmiller.com.