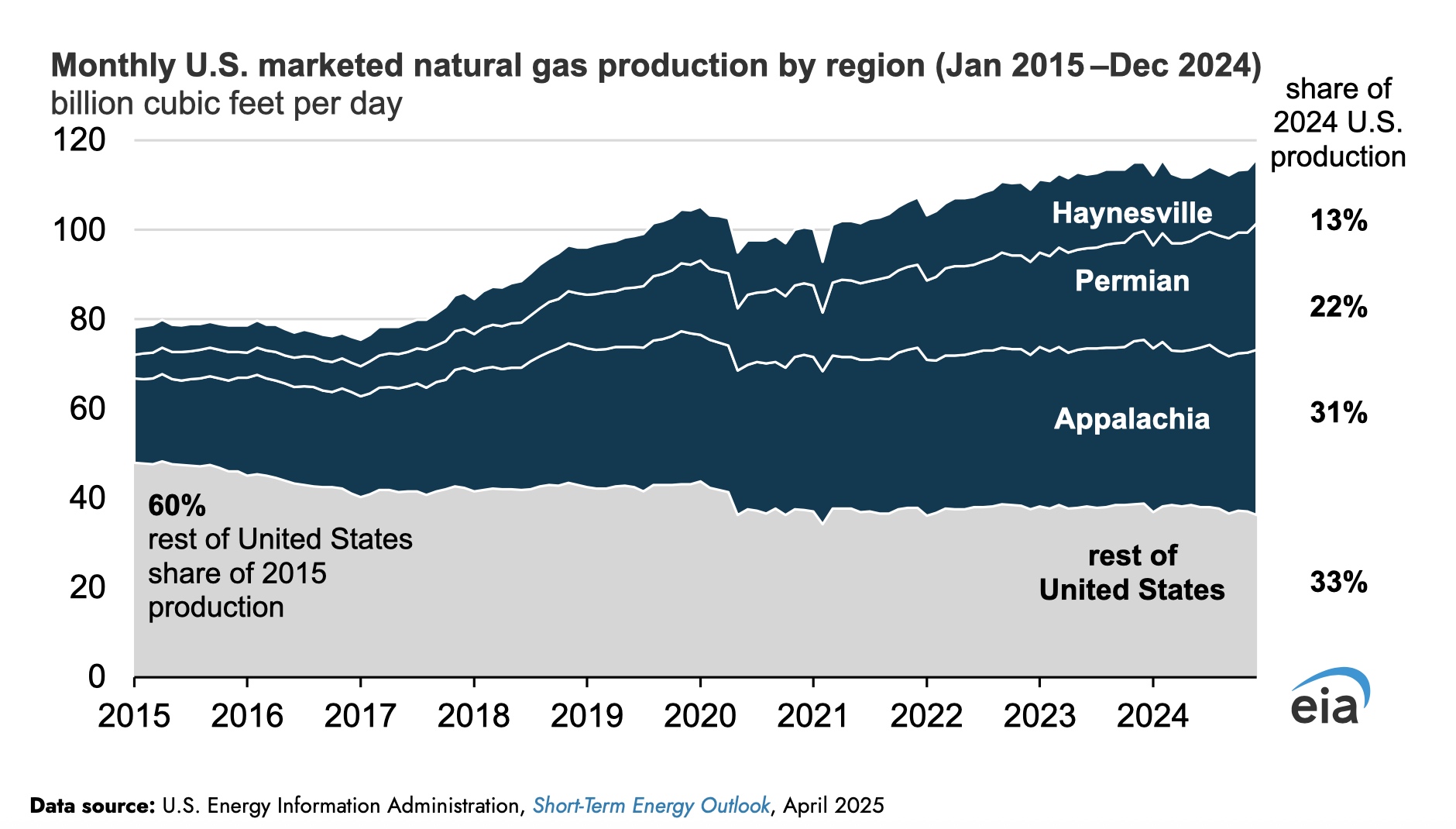

By the time 2026 arrives, the Permian Basin will again be producing more natural gas than any other region in North America. Whether that abundance translates into “bright prospects” depends on where one stands in the value chain—but the consensus among analysts is that natural gas will play a larger strategic role in the Basin’s economics than at any point in its history.

The Permian’s gas story has long been framed as a byproduct problem. Associated gas surged alongside oil drilling, overwhelming takeaway capacity and crushing regional prices. That dynamic hasn’t vanished, but it has evolved. New long-haul pipelines, rising LNG demand, and a structural increase in gas-fired power consumption are changing how operators, midstream companies, and marketers view Permian gas in 2026.

Supply remains strong—by design

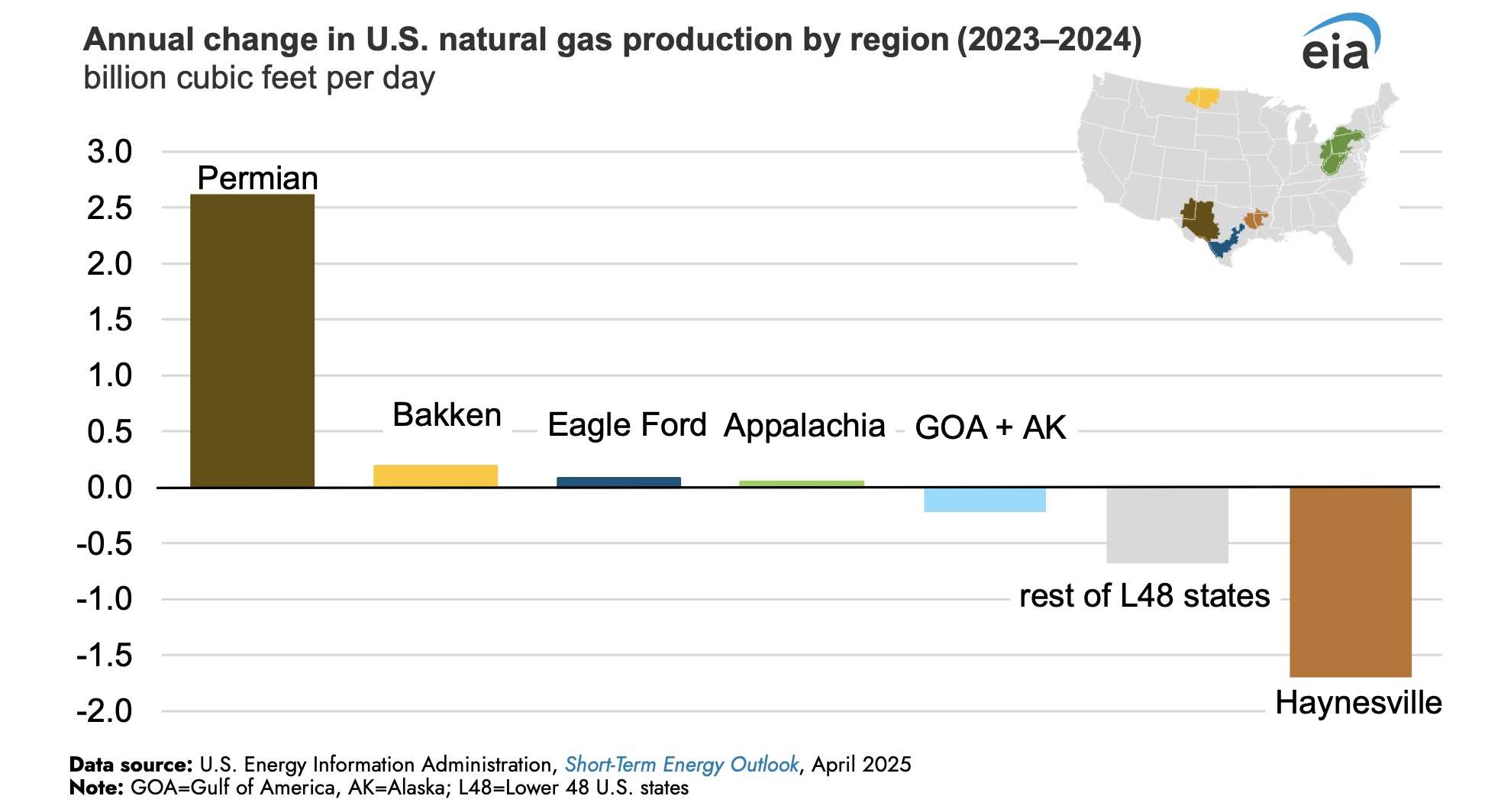

The U.S. Energy Information Administration (EIA) continues to project the Permian Basin as the largest contributor to U.S. natural gas production growth. In its Short-Term Energy Outlook, the agency notes that associated gas from oil-directed drilling will remain the primary driver of incremental supply through at least the mid-2020s. That means volumes are likely to grow even if gas prices themselves do not.

As EIA Administrator Joe DeCarolis has observed in recent outlook briefings, “Natural gas production growth is increasingly tied to crude oil economics, particularly in the Permian Basin, where oil drilling decisions effectively set the trajectory for gas supply.” For producers, that reality underscores a familiar tension: gas is plentiful, but monetization is uneven.

Demand is catching up

On the demand side, however, the picture is improving. U.S. LNG export capacity continues to expand, and Permian gas—via the Gulf Coast—feeds directly into that market. LNG developers have emphasized the importance of long-term, low-cost supply, a description that fits West Texas gas even after transportation costs.

Domestic demand is also shifting in meaningful ways. Natural gas remains the backbone of U.S. electricity generation, and its role is expanding as power demand accelerates. Data centers, cloud computing campuses, and artificial intelligence training labs are energy-intensive, around-the-clock consumers of power. While renewables are part of the mix, grid operators increasingly rely on gas-fired generation for reliability and dispatchability.

A senior analyst with International Energy Agency recently noted that “gas-fired generation is often the fastest and most scalable option to meet sudden increases in electricity demand from digital infrastructure.” In regions like Texas, where data center development is accelerating, that translates directly into stronger regional gas burn.

Price realism, not euphoria

Still, few experts expect a return to sustained, high Henry Hub prices in 2026. The market remains well supplied, storage levels are healthy, and efficiency gains continue to lower breakevens. The “bright prospects” for natural gas are therefore less about price spikes and more about volume certainty and long-term relevance.

From a Permian perspective, that matters. Gas may not rival oil as a margin driver, but it is increasingly central to project economics. Producers that once viewed gas handling as a cost center are now optimizing completions, spacing, and infrastructure to maximize gas recovery and reduce flaring exposure.

Strategic advice for 2026

For operators and service companies, several themes stand out:

- Midstream alignment matters.Securing firm transportation and processing capacity remains critical. Bottlenecks can quickly erase value in a high-volume environment.

- Electrification and emissions strategies pay dividends.Gas captured and marketed is gas not flared—and increasingly, gas with a lower emissions footprint commands better market access.

- Know your end market.Whether gas is destined for LNG, power generation, or industrial use affects contract structures and pricing risk.

The bottom line

Natural gas in the Permian Basin in 2026 is unlikely to deliver headline-grabbing prices—but it is increasingly indispensable. As oil drilling continues, LNG exports expand, and power demand from data centers and AI infrastructure rises, Permian gas is moving from byproduct to pillar. For industry professionals, the opportunity lies not in betting on price, but in mastering scale, efficiency, and market access in a gas-rich future.