The first quarter of 2026 has offered a revealing snapshot of the oilfield services (OFS) sector, as Halliburton, SLB, and Baker Hughes each reported results shaped by geopolitical disruption, shifting capital flows, and an evolving energy landscape. While all three firms delivered respectable profitability—and in some cases beat expectations—the underlying story is one of divergence: between international and North American markets, between traditional oilfield services and newer energy technologies, and between short-term disruption and longer-term opportunity.

Halliburton: Margin Strength Amid North American Softness

Halliburton posted first-quarter revenue of $5.4 billion, essentially flat year-over-year, but nearly doubled net income to $461 million, reflecting improved margins and cost discipline.

The company’s performance underscores a familiar theme for Permian-focused observers: North America remains soft, while international markets carry the growth story. North American revenue declined 4%, largely due to reduced stimulation activity and weaker artificial lift demand, while international revenue rose 3%, led by strong gains in Latin America and Europe/Africa.

Segment-wise, Halliburton’s Completion and Production division—its bread-and-butter—slipped 3% on lower pressure pumping activity, while Drilling and Evaluation grew modestly.

CEO Jeff Miller pointed to “early innings of a recovery” in North America, a comment that aligns with modestly improving rig economics but not yet a full rebound. The company also flagged Middle East disruptions as a measurable drag on earnings, highlighting how geopolitical risk is now a recurring line item rather than an anomaly.

SLB: Scale and Portfolio Cushion Volatility

SLB, still the largest and most globally diversified of the three, reported first-quarter revenue of $8.7 billion, up 3% year-over-year, aided in part by its 2025 acquisition of ChampionX.

Strip out that acquisition, however, and the picture is more subdued: underlying revenue declined roughly 7%, reflecting softness across both North America and international markets.

The ChampionX integration contributed $838 million in revenue and boosted EBITDA, reinforcing SLB’s long-standing strategy of expanding into production chemicals, artificial lift, and digital solutions—areas less tied to drilling cycles.

Geographically, SLB mirrored its peers: growth in the Western Hemisphere and offshore markets was offset by declines in the Middle East, where conflict-related disruptions curtailed activity.

More importantly, SLB continues to lean into nontraditional growth vectors, including digital platforms and data infrastructure tied to energy-intensive computing. Industry observers note that these businesses may decouple portions of revenue from rig counts, offering a structural hedge against cyclicality.

Baker Hughes: Energy Transition Strategy Gains Traction

Baker Hughes delivered one of the more intriguing quarters, reporting $6.6 billion in revenue (up 2% year-over-year) and $930 million in net income, with adjusted EBITDA rising 12%.

The standout performer was its Industrial & Energy Technology (IET) segment, which generated record orders of $4.9 billion and drove a backlog exceeding $33 billion.

This segment—focused on LNG, gas infrastructure, turbines, and decarbonization technologies—continues to reshape Baker Hughes into a hybrid energy and industrial technology company. Strong demand tied to LNG expansion and power generation for data centers helped offset a 7% decline in its traditional oilfield services segment.

Like its peers, Baker Hughes cited Middle East disruptions as a headwind, with regional revenue down sharply. But its diversification strategy is clearly paying dividends, positioning the company to benefit from both hydrocarbons and the broader energy transition.

Comparative Takeaways: A Sector in Transition

Taken together, the three reports suggest that Q1 2026 was neither a boom quarter nor a bust. Instead, it fits the profile of a transitional period—strong profitability supported by disciplined capital management, but uneven demand across regions and service lines.

Several key themes emerge:

- International resilience vs. North American caution.All three companies saw stronger performance outside the United States, while North America—particularly pressure pumping—remains subdued.

- Middle East disruption as a systemic factor.Conflict in the region reduced activity and trimmed earnings across the board, reinforcing geopolitical risk as a persistent operational variable.

- Diversification is paying off.SLB and Baker Hughes, in particular, are benefiting from exposure to chemicals, digital services, LNG, and power infrastructure—areas less tied to drilling cycles.

- Margins matter more than growth.Halliburton’s earnings surge despite flat revenue illustrates the industry’s current emphasis on capital discipline over volume expansion.

Outlook: Cautious Near Term, Constructive Longer Term

Looking ahead, the remainder of 2026 appears likely to unfold in two phases. The near term may remain choppy, as operators hesitate to ramp drilling despite higher oil prices, partly due to cost inflation and geopolitical uncertainty.

However, the medium-term outlook is more constructive. Supply disruptions and energy security concerns are expected to drive increased upstream investment, particularly in North America and LNG projects.

For OFS firms, that translates into a gradual recovery in core service lines—completions, drilling, and evaluation—while newer segments such as gas infrastructure, power systems, and digital services continue to expand.

Implications for the Permian

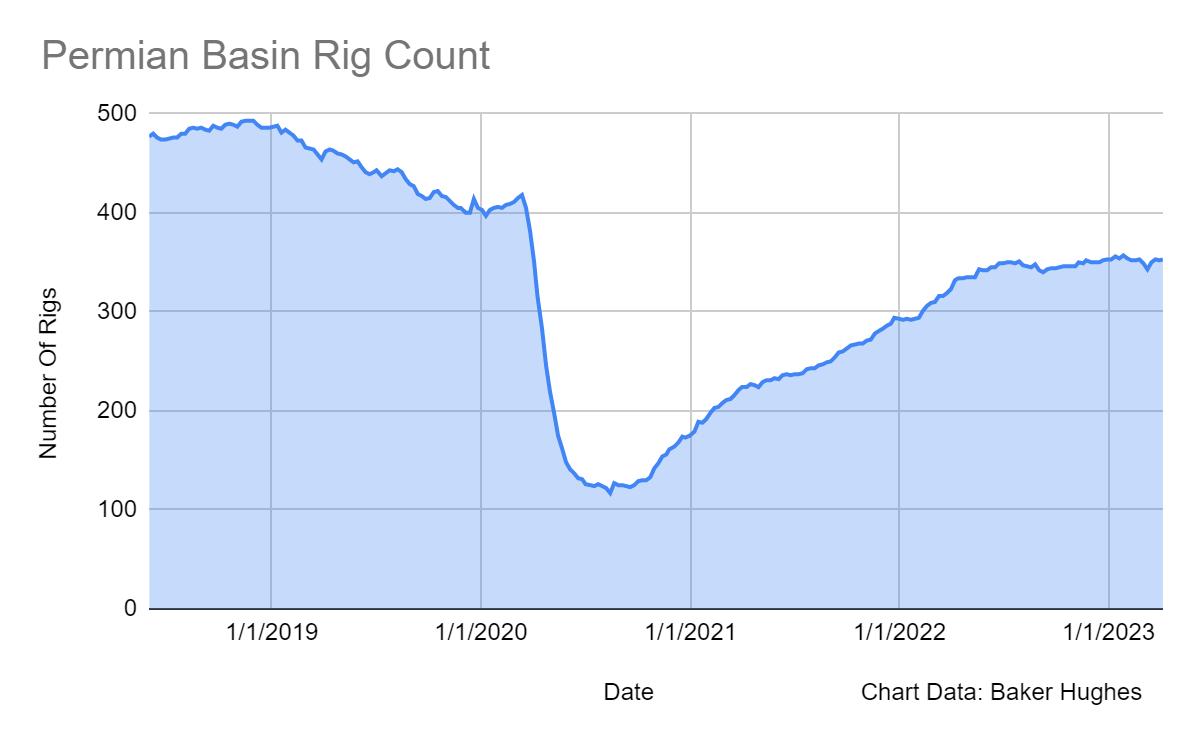

For Permian Basin stakeholders, the message is nuanced but actionable. Traditional service lines tied to shale completions may recover, but not explosively. Meanwhile, opportunities are emerging in adjacent sectors—natural gas infrastructure, electrification, and data-center-driven power demand—that are increasingly intersecting with oilfield expertise.

In short, the “Big Three” are signaling that the OFS industry is no longer defined solely by rig counts. The companies best positioned for the next cycle are those building portfolios that can thrive whether the barrel trades at $60 or $100—and whether the growth comes from wells, wires, or watts.