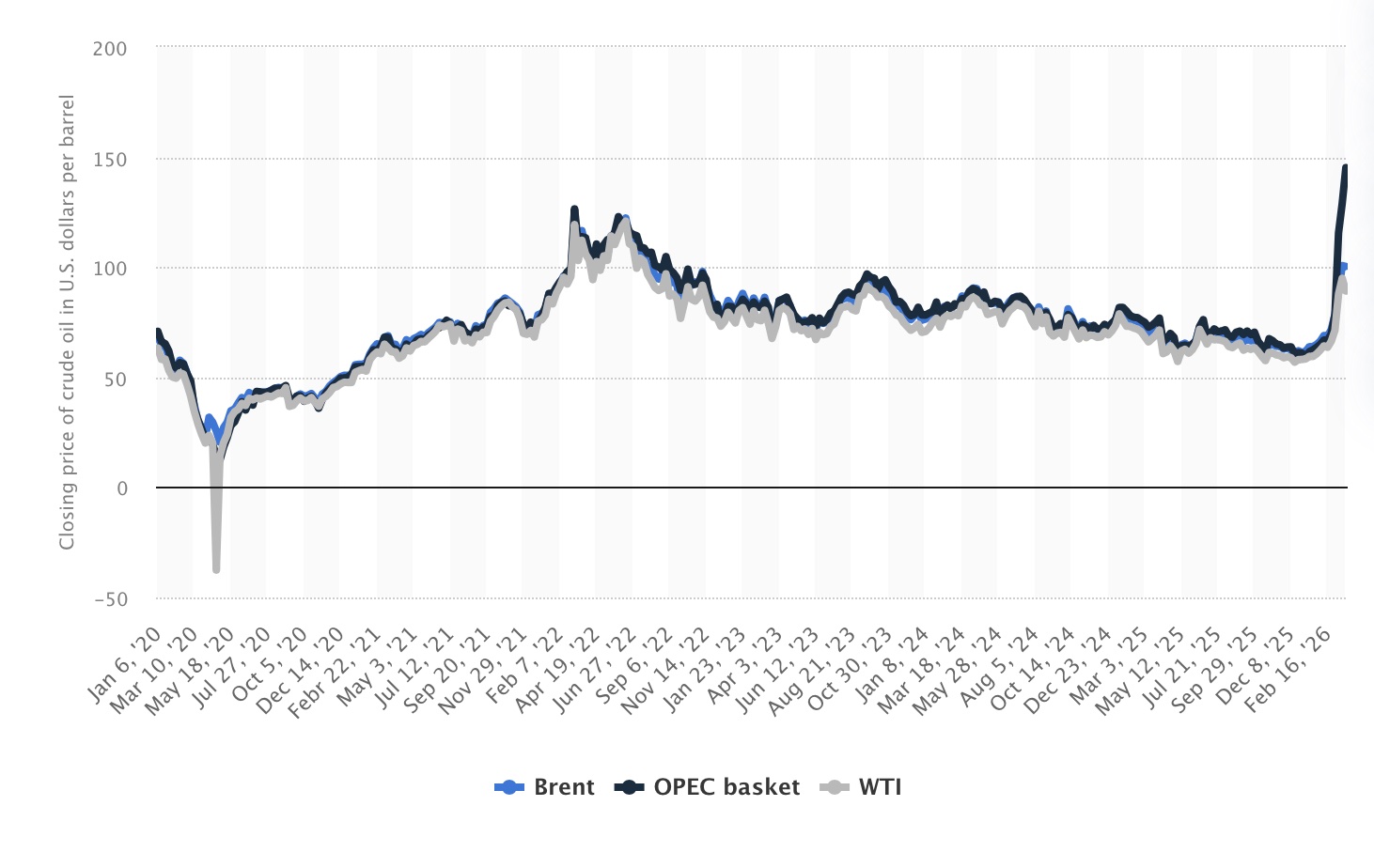

As I write these words (2:00 p.m. on Friday, March 27), WTI crude stands at $99.48. And note that we are talking WTI here, not Brent. Brent was at $113. And this in a world where, only a few months ago, forecasters were saying we’d be in the $50s range at this time. What a difference a volatile March can make.

While I’m looking up these figures on OilPrice.com, I see this headline: “U.S. Drillers Pull Back as WTI Soars Past $98.”

Pull back? But yes. Here’s the lead from that piece:

“The total number of active drilling rigs for oil and gas in the United States fell this week, according to new data that Baker Hughes published on Friday, bringing the total rig count in the US to 543, down 49 from this same time last year. The number of active oil rigs fell by 5 to 409 during the latest reporting period, according to the data. This is 75 below this same time last year. The number of gas rigs fell by 4, sinking to 127, which is 24 more than this time last year. The miscellaneous rig count stayed the same at 7.

“The latest EIA data showed that weekly U.S. crude oil production fell for the fifth week in a row during week ending March 20. US crude oil production averaged 13.657 million bpd during the reporting period—a 11,000 bpd dip from the week prior, and 205,000 bpd under the all-time high.”

None of his lethargy would be odd if we things had followed the course set in 2025 and earlier—a long, steady decline in prices. But the O&G world experienced a shakeup.

In early March, global oil markets were jolted by a geopolitical shock few had fully priced in: the near-closure of the Strait of Hormuz amid escalating conflict in the Persian Gulf. The disruption—affecting roughly 20 percent of the world’s oil flows—sent crude prices surging past $100 per barrel, briefly reaching as high as $120–$125 in volatile trading.”

For the Permian Basin, the implications are immediate—and potentially transformative.

A Supply Shock with Global Reach

The Strait of Hormuz is not just another chokepoint. It is the central artery of global oil trade, through which millions of barrels per day move from the Middle East to Asia, Europe, and beyond. When tanker traffic effectively collapsed in early March, global supply tightened almost overnight.

Markets responded accordingly. Prices climbed more than 50 percent in a matter of weeks, with analysts warning that further escalation could push crude toward $150 or higher in extreme scenarios.

For U.S. producers—particularly those in the Permian Basin—this is a classic case of geopolitical risk translating into domestic opportunity.

What Higher Prices Mean for Permian Producers

At $100-plus oil, nearly every producing well in the Permian Basin is profitable, and many become highly lucrative. Breakeven levels across the basin typically fall in the $40–$60 range, meaning today’s pricing environment significantly expands margins.

In practical terms, that creates three immediate effects:

- Cash Flow Surge.

Operators are seeing stronger free cash flow, improving balance sheets, and enabling shareholder returns—whether through dividends, buybacks, or debt reduction.

- Inventory Revaluation.

Previously marginal drilling locations suddenly become economic. This effectively expands the basin’s recoverable reserves without drilling a single new well.

- Measured Response from Operators.

However, unlike past cycles, operators are not rushing headlong into aggressive drilling. Early indications suggest many are waiting to see whether elevated prices will prove durable before committing to large capital increases.

That restraint reflects hard-earned lessons from the boom-and-bust cycles of the past decade.

How Long Could Prices Stay Elevated?

The key question for Permian decision-makers is duration. Current market analysis suggests three broad scenarios:

Short-Term Disruption (Weeks).

If the Strait reopens quickly and flows normalize, oil could fall back into the $80–$90 range within a matter of months.

Intermediate Disruption (1–3 Months).

Partial restoration of shipping—with lingering risk—could keep prices in the $100–$110 range before gradually easing.

Extended Crisis (Several Months).

A prolonged closure or escalation could drive prices into the $130–$150 range or higher, with extreme cases approaching $200.

Even in the most optimistic case, analysts note that markets will not “snap back” immediately. Physical oil supply chains take time to normalize, meaning elevated prices could persist even after the Strait reopens.

Natural Gas: A Different Story

While oil markets are globally integrated, natural gas markets remain more regional. The U.S., buoyed by abundant domestic supply, has been largely insulated from the worst of the global gas price spike.

Despite severe disruptions to LNG flows through the Strait, U.S. natural gas prices have remained relatively stable, with storage levels and production offsetting international volatility.

For Permian operators, this reinforces a familiar dynamic: oil drives near-term upside, while gas remains a longer-term infrastructure and export story.

Opportunities for the Permian Basin

The current environment presents several strategic opportunities for operators, service companies, and midstream players.

Capitalize on Pricing—But Stay Disciplined.

The temptation to ramp drilling is real, but companies that maintain capital discipline may ultimately capture the most value if prices prove temporary.

Accelerate DUC Completions.

Bringing drilled-but-uncompleted wells online offers a faster, lower-risk way to capitalize on high prices without committing to full-cycle drilling programs.

Strengthen Midstream and Export Positioning.

As global buyers seek non-Middle Eastern supply, U.S. crude—particularly from the Permian—becomes more attractive. Gulf Coast export infrastructure stands to benefit.

Service Sector Rebound (Eventually).

While service companies may see a lag as operators hesitate, sustained high prices would ultimately drive increased demand for rigs, crews, and completion services.

Geopolitical Premium as a Structural Tailwind.

Even after the crisis subsides, markets may assign a higher risk premium to oil prices, reflecting the vulnerability of global supply chains. That could support a higher price floor than previously expected.

Meanwhile, what about the services sector? Clearly, the spike in prices is a windfall for producers—the E&P companies. Their oilfield counterparts, the businesses in the services sector, do not stand to benefit so directly. For them, revenue gains must come from largesse that is passed through from the E&Ps. Ordinarily, that happens when drilling ramps up. When drilling intensifies, demand for the work of service companies intensifies with it, and in that shift the service companies find leverage to demand higher rates. But in this odd blip we find ourselves in, with the exploration companies holding the line, service companies likely will not have much bargaining power to improve their positions. It’s been a tough year—make that multiple years—for the services sector.

But back to the news of the moment:

A Moment of Advantage—With Caveats

For the Permian Basin, the Hormuz disruption is, in many ways, a reminder of its strategic importance. At a time when one-fifth of global supply is at risk, the United States—and particularly the Permian—offers stability, scale, and responsiveness.

But the opportunity comes with caution.

Geopolitical spikes have historically been short-lived. Prices rise quickly—but they can fall just as fast when tensions ease. And in today’s market, with investors demanding returns over growth, the industry’s response is likely to be more measured than in past cycles.

Still, for now, the message is clear: when the world’s most critical oil artery falters, the Permian Basin becomes that much more indispensable.