Enverus Intelligence Research (EIR), a subsidiary of Enverus, an energy-dedicated SaaS company, released in mid-October its summary of 3Q24 upstream M&A activity. Following 12 months of heightened consolidation in oil and gas, the pace of deals significantly slowed in the third quarter of 2024, with $12 billion in announced deals, the lowest quarterly total since 1Q23. The drop in M&A value was largely attributable to a pause in public company consolidation as well as fewer deals to be had in the prolific Permian Basin.

“Upstream M&A was bound to drop after the unprecedented lift of corporate mergers and private equity exits since 2023. Those deals raised asset prices and cut the number of potential targets,” said Andrew Dittmar, principal analyst at EIR. “An additional factor could have been increased volatility in crude prices during the third quarter. Any time commodities get more volatile, oil and gas deals are harder to negotiate. However, that is a short-term turbulence until buyers and sellers feel more confident on the direction oil prices are moving.”

The most notable shift in the just-completed quarter was the lack of consolidation between publicly traded E&Ps, the first time that has happened in a quarter since 2022. The $188 billion in public company consolidation since the start of 2023, with 11 public deals over $2 billion, leaves significantly fewer targets to pursue. In addition, large buyers like Chevron, ConocoPhillips, Diamondback Energy, and ExxonMobil have been busy closing and integrating deals, with timelines often delayed by extra anti-trust scrutiny by the Federal Trade Commission.

“While corporate M&A has slowed, the industry is not done consolidating. If you look out a few years from now, there are going to be fewer companies operating in the main U.S. shale plays,” said Dittmar. “However, the path to get there may be a bit bumpier from this point. The most obvious deals in terms of a good strategic fit between assets and a ready seller got done earlier in the consolidation cycle. Buyers may need to offer higher premiums than the average 15 percent paid to selling companies so far to tempt some of these remaining companies into a deal. However, that needs to be balanced against not overpaying and still striking a deal that also makes sense for the acquirer.”

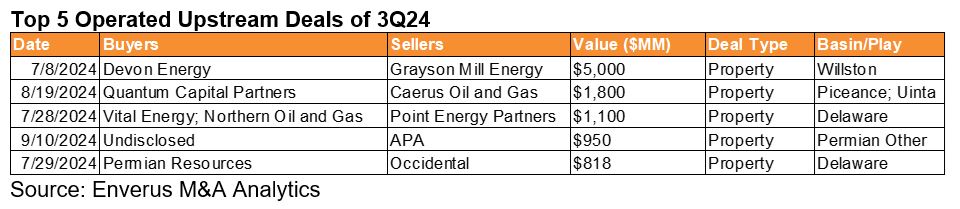

While the market waits for further corporate consolidation, asset deals by public companies are likely to play a more prominent role in upstream M&A. Companies that were buyers are now likely to sell parts of the combined portfolios. APA, which purchased Callon Petroleum in early 2024, has already been active on that front, selling a portfolio of Permian conventional assets for $950 million to a private buyer. Occidental also sold off a piece of its Delaware Basin position to Permian Resources for $818 million after closing the CrownRock acquisition. Future non-core sales by public companies could target lower quality or extensional areas of the Permian, the Mid-Continent, and areas like the Uinta Basin, where Ovintiv has been reported to be shopping its position.

Sales by private equity companies are also likely to continue to feature prominently in upstream deal activity, with a larger focus outside the Permian Basin, where there are more remaining opportunities and pricing for undeveloped drilling inventory is more reasonable. The largest transaction of 3Q24 was Devon Energy’s acquisition of EnCap-funded Grayson Mill Energy in the Williston Basin for $5 billion. Areas like the Williston and Eagle Ford, where private companies like Verdun Oil and WildFire Energy operate, offer the chance for buyers to get larger chunks of undeveloped inventory for less money per location, even if the inventory isn’t as economic to drill as the core Permian assets that sold earlier.

“Ideally, in a transaction, the buyer wants to improve the overall quality of their inventory portfolio and lengthen the years of total inventory they have to drill,” said Dittmar. “However, with the remaining opportunities that is going to be challenging to do at a reasonable price. Instead, you are going to see buyers pick up bigger chunks of middle-quality inventory or buy small pieces of high-quality drilling opportunities that go right to the front of the line for development. That is what Vital Energy did with its acquisition of Point Energy in the Delaware Basin. The deal added locations that are competitive with the best inventory Vital has left to drill, even if there wasn’t that much total inventory associated with the asset.”

While private equity has featured most prominently in deal markets as a seller of shale inventory to public companies, these firms are still raising new capital and putting it to work, but at a slower pace than before 2020. With fewer opportunities to get into the main shale plays, private firms are broadening the search to areas without competition for deals from public companies. That is also leading to more private-to-private transactions between groups that have been invested for a lengthy time to ones that have raised fresh capital. And example is he sale of Caerus Oil and Gas, which operates gas assets in Colorado’s Piceance Basin and Utah’s Uinta Basin, to Quantum Capital Group for $1.8 billion.

“There is still a significant amount of oil and gas to develop outside the main shale plays focused on by bigger public companies,” Dittmar said. “In some cases, like the Piceance Basin, the economics aren’t compelling to public companies that have higher-return drilling opportunities elsewhere. In other cases, like western Oklahoma assets or the Northwest Shelf of the Permian, there are pockets of economic inventory but not enough scale to interest the larger public E&Ps. We’re going to see more interest in these types of assets from private companies and small public companies locked out of the better-known plays. That includes an IPO pipeline for new, small public companies that is busier than it has been in years. Now that the big shale plays are increasingly consolidated, the industry is dusting off maps and rediscovering areas that have been under the radar for the last decade.”