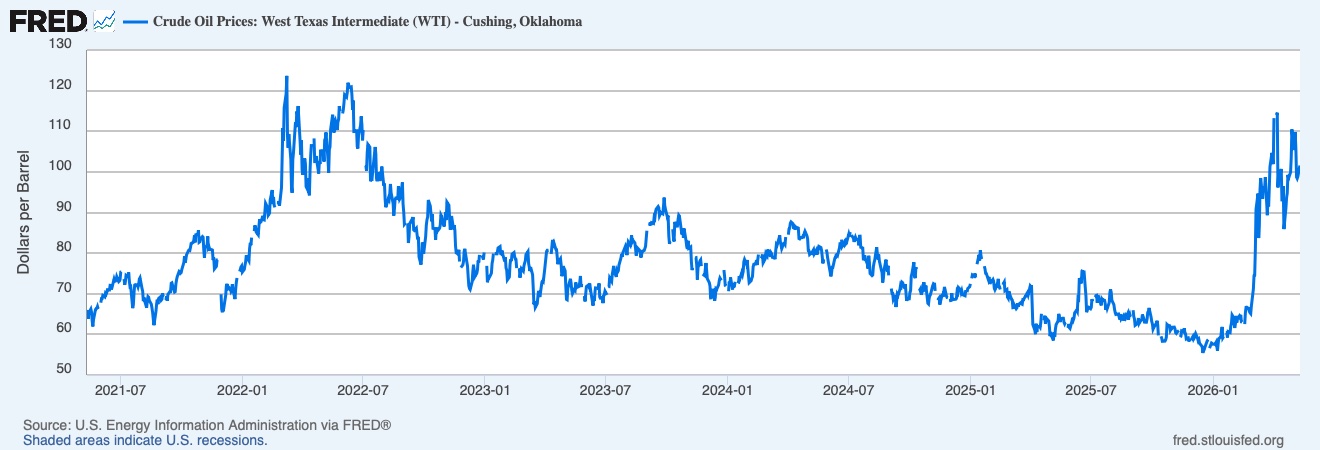

With the huge uptick in O&G commodities prices since early February, who has benefited most

The winners are emerging, certainly, but they are not evenly distributed across the oil patch.

The sudden rise in oil and natural gas prices since early February has created a familiar but uneven phenomenon in the energy business: a rush of cash toward producers, traders, and investors, while much of the service sector waits for its share to arrive.

For the Permian Basin, the spike has acted less like a rescue and more like an accelerator. Many operators entered 2026 leaner and more disciplined than in past boom cycles. When geopolitical tensions in the Persian Gulf abruptly lifted crude prices well above expectations, Permian producers were positioned to capitalize quickly.

But not everybody is benefitting equally.

The clearest winners so far appear to be low-cost exploration and production companies—especially those with substantial unhedged production. Firms that had little or no downside price protection in place have enjoyed immediate upside exposure as West Texas Intermediate (WTI) prices climbed sharply higher.

By contrast, heavily hedged producers are participating less dramatically in the rally because portions of their production remain locked into earlier, lower-price contracts. In effect, some companies protected themselves against the low-price environment many analysts expected for 2026, only to see the market move strongly the other direction.

That dynamic may begin changing later this summer.

As hedge contracts gradually expire, more Permian producers could gain direct exposure to elevated commodity prices. If crude remains firm into the third quarter, many companies may begin realizing significantly larger margins than they are capturing today. The result could be another wave of free cash flow, debt reduction, stock buybacks, and consolidation activity.

Meanwhile, hedge funds and commodity trading firms may actually be among the largest short-term beneficiaries of all.

Periods of geopolitical volatility create ideal conditions for sophisticated trading operations. Commodity funds positioned correctly ahead of the Persian Gulf disruption likely generated outsized gains not only from crude itself, but also from options, futures spreads, natural gas, refined products, and energy equities. Some trading houses prosper during volatility regardless of whether prices rise or fall, provided the swings are large enough.

That reality highlights an important distinction: producers profit from selling hydrocarbons, but trading firms profit from movement itself.

For oilfield service companies, however, the story is more complicated.

Despite stronger commodity prices, the expected drilling boom has not fully materialized. Producers remain cautious after years of investor pressure demanding capital discipline. Many operators appear reluctant to launch major drilling expansions based solely on a geopolitical event that could ease later this year.

As a result, service companies in the Permian Basin may not yet be sharing proportionally in the current largesse. Pressure pumping firms, drilling contractors, and completion providers are seeing steadier conditions and firmer pricing in some categories, but not the runaway growth that characterized earlier shale booms.

That could change if high prices persist into the second half of 2026.

Should operators gain confidence that elevated prices will hold, activity levels could rise materially, particularly for completion crews, artificial lift providers, and production optimization firms. Until then, many service companies remain in a “wait-and-see” posture while E&Ps harvest the immediate financial rewards.

If, in fact, prices remain “higher for longer” and drilling activity picks up, service companies will gain some bargaining leverage and potentially can negotiate some better terms.

The Permian Basin itself remains exceptionally well positioned in this environment.

Globally, few producing regions can respond to higher prices as quickly as the Permian can. Existing infrastructure, enormous drilling inventories, export connectivity, and relatively low breakeven costs give the Basin advantages that many international competitors cannot easily match. Domestically, the Permian continues functioning as America’s primary swing production engine.

Natural gas may become an equally important part of the story. Associated gas volumes, LNG export demand, and electricity needs tied to artificial intelligence and data centers are all strengthening the long-term strategic importance of Permian production.

For now, though, the immediate answer to the question “Where’s the money going?” is fairly straightforward:

First to producers.

Second to traders.

And only later—perhaps—to the rest of the oilfield.