The Beatles sang about a “Long and Winding Road” leading to their fame and fortune, and what is now the world’s top-producing oil basin—the Permian—has a similar tale. In this story experts from research firms S&P Global and Wood Mackenzie help unpack the deep and wide layers of the Permian’s national and global significance.

In the Beginning

It was W. H. Abrams #1 in July of 1920 that first hinted of oil riches hiding under the arid plains of the area now known by the name of its subsurface geological age, the Permian Basin. Some Texas historians argue that this area is actually the south end of the Llano Estacado. Indeed, early settlers knew nothing of any Permian geological age miles beneath them. But 1920 was when the Permian name began flowing to the surface.

The big strike came almost three years later. Santa Rita #1 on May 8, 1923, proved to everyone that what was under the ground was worth exponentially more than the cotton fields struggling on the top side.

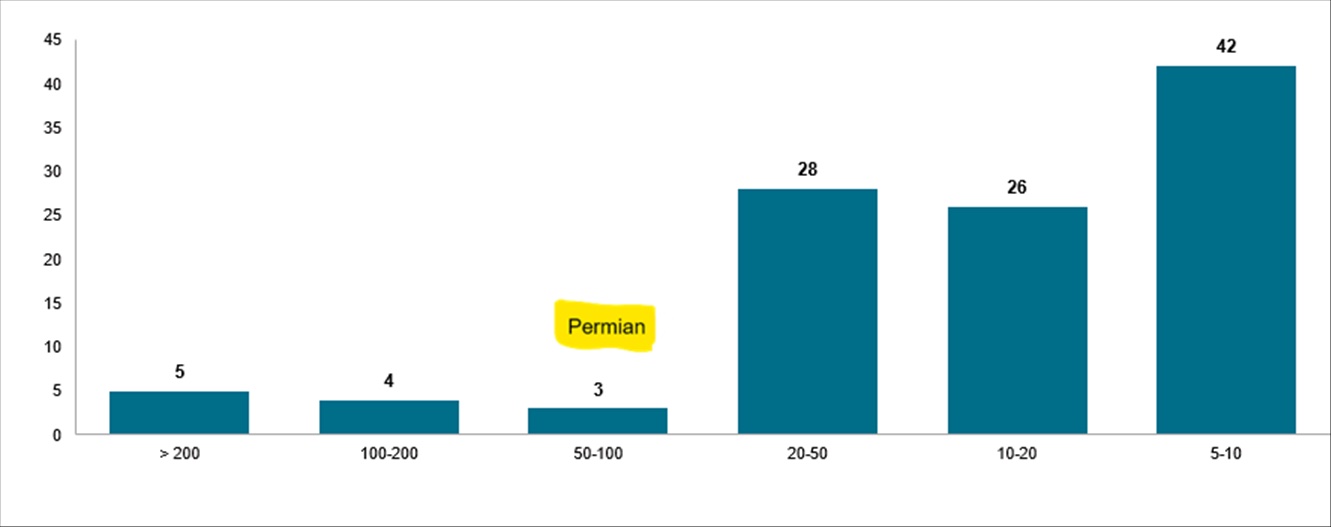

For this chart on exports, the vertical axis represents number of fields and the horizontal axis is “fields in billions of barrels equivalent (BOE) in groupings.” Source S&P Global

Rebirth

Now let’s fast forward 90 years to 2010. In between, the Permian had helped the United States and its allies win World War II, as neither Germany, Japan, nor Italy had any significant energy resources. But by 2010 the Permian’s dominance had seemed to end. Production had steadily declined since 1971, as the best of the then-known conventional reservoirs had been drained of most of their accessible oil.

But by 2010 the shale revolution had become exactly that—an out-with-the-old, in-with-the-new process for producing the tight shales that had been out of reach before hydraulic fracturing and laterals became everyday words.

In 2011, Permian production surpassed 1 million barrels per day for the first time since 1998, and by 2025, daily production averaged 6.62 million BBL/d, according to the U.S. Energy Information Administration (EIA).

In 2019 the Permian surpassed Saudi Arabia’s giant Ghawar field to become the single most productive basin in the world. With that, and with help from other shale-powered regions, including most prominently the Bakken and Eagle Ford, the United States leapfrogged Saudi Arabia to become the world’s leading oil producer.

Place in this World

Let’s put the Permian in perspective: If its 66 counties were a separate nation, it would rank third in the world in oil production and fifth in the world for natural gas production. And of those 66, just 10 counties account for most of that: In Texas, Martin, Midland, Andrews, Glasscock, Howard, Loving, Reagan, and Ward; In New Mexico, Lea and Eddy.

Supersize Me

Bob Fryklund

Certainly, in today’s energy market, in flux from the situation with Iran, the United States is even more dependent on the Permian for stability than any time in recent memory.

Bob Fryklund, chief upstream strategist for global research firm S&P Global, says the Permian’s dominance arises from its being among the biggest in size—width and depth—in the world. “It’s one of only 12 basins in the world [of its size], and that’s pretty doggone unique.”

Fryklund remembers personally how radically things have changed. After graduating from university, he worked in Oklahoma’s Mid-Con area in the 1980s, but had friends sent—or maybe sentenced—to the Permian. “In those days, we thought that was the graveyard,” he laughed.

It’s all different now, with the Permian in its own version of the Big 12, “Based on the size and billions of BOE. There are nine fields bigger than the Permian. Those fields are dominantly in the Middle East,” he said. “And there’s also in Russia, in Siberia. The Eastern Maturin in Venezuela is another one.”

But none of those is producing 6 million barrels per day, with the potential for much more. Said Fryklund, “We still expect the Permian, just liquids, to get over 8 million barrels a day. And that should be by 2029.”

Deep and Wide

The Permian’s pay zones stretch in many directions. “It’s up and down, this huge column of potential…. I think that was what was underestimated for so many decades,” Fryklund mused, with much of the deeper plays released in the shale revolution.

Worldwide

Perhaps the biggest break for the region was the December 18, 2015, repeal of the 40-year-old ban on exports, signed into law by President Obama in the Consolidated Appropriations Act, 2016. The ban had begun in the 1975 Energy Policy and Conservation Act, a response to the 1973–1974 Arab oil embargo and severe fuel shortages. It prohibited exporting domestically produced crude oil to boost national energy security and conserve supply.

But by 2015, domestic production in the shale plays had flooded the U.S. market and crashed prices. There was no longer a need to hoard oil for national security purposes—instead it could be exported to reduce trade deficits and give shale drillers a market. Fryklund noted that S&P’s predecessor, IHS Markit, wrote position papers supporting the ban’s repeal.

Scott Norlin

A previous PB Oil and Gas story discussed the Permian’s place in LNG exports, and Fryklund noted that most of those come from Appalachia, but, added Scott Norlin, senior research manager for research firm Wood Mackenzie, “The Permian is producing roughly 20 bcfd today. U.S. LNG exports look to grow to nearly 40 bcfd. Export economics wouldn’t be as attractive if the U.S. gas market didn’t have low-to-no-cost associated Permian gas to put downward pressure on Henry Hub.” Fryklund also noted the advantages of Permian gas because it is almost “free” as a byproduct of oil production.

Light and Sweet vs. Heavy and Sour

Export options solved another issue, which is that there is a limit to how much light, sweet WTI (West Texas Intermediate) oil U.S. refiners can handle. They need at least a certain amount of the heavier crude from the Middle East, Canada, and Venezuela (more on that later) to make product. So, this relieved pressure to take on more WTI than they preferred, because it could now be shipped elsewhere.

Adjustments in the refining balance are something Fryklund has lived through personally. In his previous decades with a vertical major, declining U.S. production created concerns among many refiners dealing with “a calculated risk that, long term, we were going to be short on light and that we’re going to be long on heavy. So, the refineries in the Gulf Coast and in India were changed over and made to handle those complex crudes” instead.

But then suddenly in 2009, the shale plays began flooding the market with light sweet, “And that changed what’s available on the Gulf Coast for refiners,” he said.

The negatives for just running light sweet are economic. Heavier crude often provides better economics due to its density and its ability to produce more refined product, especially jet fuel.

Enter the Iran and Venezuela Issues

In March of this year, 20 percent of the world’s oil and a similar percentage of its LNG was bottled up at the Strait of Hormuz. More than 600 tankers at one time were stuck, said Fryklund. Although there was some increased flow through Saudi Arabia’s East West pipeline, which delivers crude to its western ports, located beyond the Strait, its 3 million barrels per day are not enough to make up all the difference—and it is no help to stranded LNG.

Much of that is heavy oil, but Venezuela—which is not behind the Strait of Hormuz and produces very heavy crude—is no longer sanctioned regarding crude sales. CNBC and others have reported that a tranche of 30-50 million barrels of Venezuelan oil will be sold by the United States, most or all of it to U.S. markets.

The Basin’s Future

“All good things come to an end,” we’ve heard from Nelly Furtado and a host of others over the decades. Is that on the horizon for the Permian?

In Fryklund’s words, “Is the Permian running out of [oil]? Eventually, yes. Anytime soon, no, not in our book.”

That’s because there are still new wells to be drilled, and current technology leaves a lot down there, especially unconventionals, which leave up to 90 percent in place.

Still, just staying even will take a lot of work, he said.

How much is a lot? How about “we have to drill basically the equivalent of another UAE, another 4 million barrels, another Brazil. We do that every year just to stay even.”

Whew!

The good news is that S&P sees more than that happening in the next couple of years, just with onshore lower 48—not counting Alaska and the Gulf.

Norlin noted that his organization does see overall U.S. production dropping in the next couple of years, but the Permian’s continued growth slows that down. “The Permian is still growing because of its superior position on the cost curve,” he said.

How long can that last? It is important to remember, Fryklund noted, that the Permian has already been declared dead once, and two things happened to breathe new life into it.

Higher prices and advances in technology.

For most of the 1980s and all of the 1990s, oil prices were barely in double figures at times. Even fracturing alone might not have helped that. But in the early 2000s, prices rose from $20 and $30 ranges to $50. Around 2005 one retail developer in Midland was quoted saying, “$50 a barrel oil floats all boats.” From there it careened between $150 and back into lower ground, before steadying.

Then unconventionals took off, reaching tens of millions of barrels of previously unavailable oil, and massive stores of natural gas. Fryklund sees other new technologies, perhaps less dramatically, pushing the recoverable oil boundaries even further.

Prices are up, at this writing, but for how long? An Iran-based peak price is not enough to spur new drilling because, as he pointed out, “The dependable price of oil has a lot to do with it too. I don’t really see anybody ramping up drilling right now, because we got $90 a barrel [for possibly just a few weeks].”

Sooooo…..

Politics also play a part, and future administrations may or may not be as oil-friendly as the current one. Still, almost all predicting agencies, domestically and worldwide, see fossil fuels not only not diminishing, they see them actually continuing to grow in demand, in some views, for decades.

With Mark Twain, the Basin may therefore declare: “The report of my death was an exaggeration.”

A longtime contributor to PB Oil and Gas Magazine, Paul Wiseman is an energy industry freelance writer.